Wealth creation is all about satisfying the curiosity to understand how the money world works, and how it can be made to work for you. In this section, you will find some video tutorials, and documents on popular questions asked about the challenges of financial planning:

Assumptions: Approximate age: 25 to 39

You are now early into your career, earning enough to be able to start saving money on a regular basis.

At this point in your career, your future objectives and major expense requirements are beginning to materialise. Top of the priority list would be to ensure you can buy your own home, with a fair mortgage interest rate. Your savings should now start expanding beyond a simple emergency cash pot, with a focus on retirement savings, followed possibly by college funds if you have children and if university fees are a consideration. Next there will be more medium and short-term goals, for instance buying or upgrading your home or car.

Generally speaking, the longer you are prepared to lock away your money, the greater its ability to compound and accumulate. Once you have an idea of your desired income in retirement, you will know whether there is a shortfall, and can plan to save to plug this gap. Remember, retirement income may not just be needed to cover your living expenses, but may also need to stretch towards elderly care, fast becoming another major expense as we live longer. Therefore, whatever you think you’ll need, increase it.

A portfolio should be created out of your ongoing disposable income, after living costs, after clearing high-interest debt and after setting aside potential tax money.

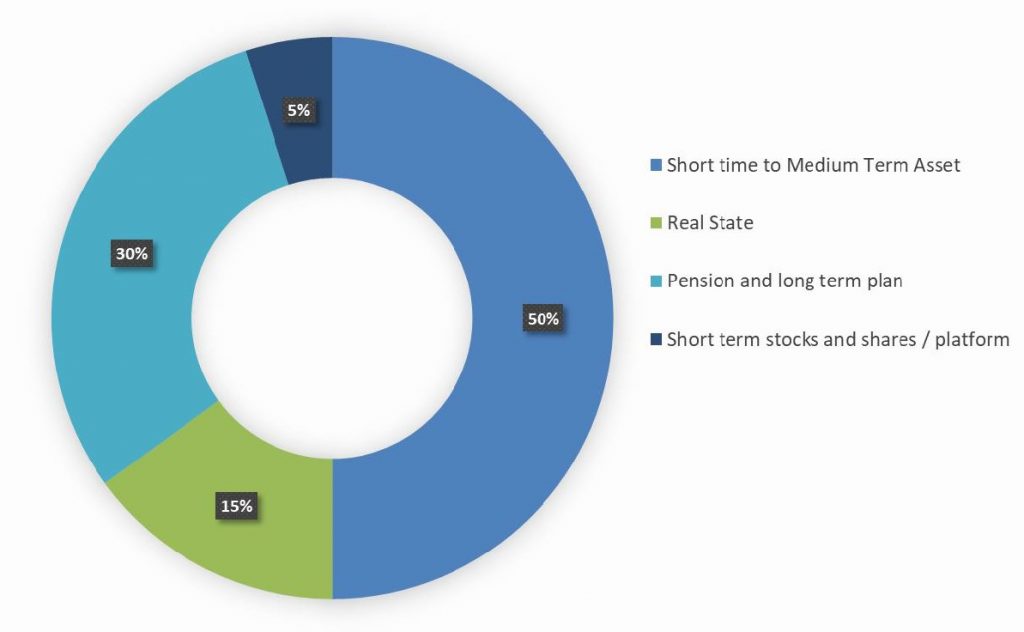

The chart below shows how your portfolio should typically be divided at this stage:

50% – Short term to medium term assets (short 2-5 years, medium 6-12 years)

15% – Real estate, including REITs and real estate crowdfunding (not including primary home)

30% – Pension and long-term plan

5% – Short term stocks and shares / platform.

Short-term assets include:

- Fixed interest accounts

- Lending clubs / peer-to-peer lending

- Short-term government bonds

- Regulated bank or government backed savings initiatives, preferably tax friendly

- Money market mutual funds

- National bonds (if living in a developed country)

- Stocks and shares on a trading platform

Medium-term assets include:

- Physical property with focus on capital appreciation or REITs

- Equity and bond funds

- ETFs

- Structured notes

Pensions and long-term assets include:

- Mutual funds – with focus on equities and bonds

- Physical property with a focus on high appreciation and rental income

- REITS

- Government backed, tax-free savings initiatives such as ISA in UK.

Assumptions: Approximate age: 40 to 59

You are now early into you highest earning years. Having erased most if not all high-interest debt, your disposable income should allow you to build on the foundations laid during your earlier years. However, you may now have young dependents, so keeping a very close eye on spending, with a determination to save each month should be a high priority.

By this age, you should be firmly on the property ladder, with mortgage repayments being comfortably made. Your emergency cash pot should be healthy. Top of the priority list now would be (should be) building up a pension income, followed possibly by college funds if you have children and if university fees are a consideration. Your short-term cash should be enough to take care of any major costs within the next 2 to 3 years, for instance home repairs or a new car.

Generally speaking, the longer you are prepared to lock away your money, the greater its ability to compound and accumulate. Your desired retirement income will now be clearer, as you will have an idea of the lifestyle you’ll want and of how inflation may impact the value of your money between now and then. You’ll be able to make a rough forecast on current private and state pension income, and you will also have an idea of what other assets you have now which can be used to generate pension income. Your focus will be to now hit and even exceed that target, to overcompensate for unexpected costs.

A portfolio should be created out of your ongoing disposable income, after living costs, after clearing high-interest debt and after setting aside potential tax money.

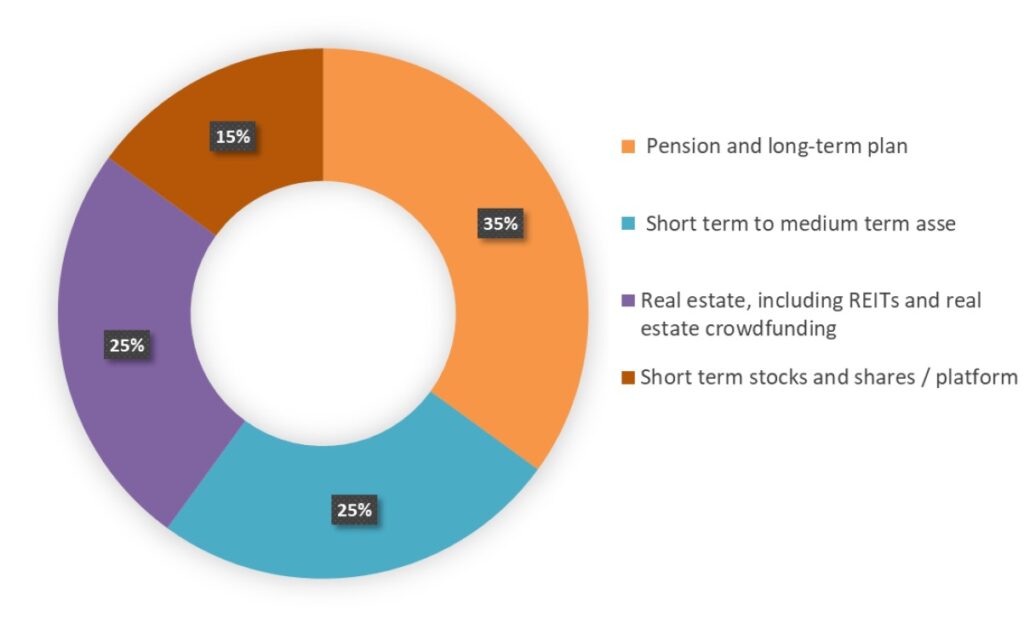

The chart below shows how your portfolio should typically be divided at this stage:

35% – Pension and long-term plan

25% – Short term to medium term assets (short 2-5 years, medium 6-12 years)

25% – Real estate, including REITs and real estate crowdfunding (excluding primary home)

15% – Short term stocks and shares / platform

Short-term assets include:

- Fixed interest accounts

- Lending clubs / peer-to-peer lending

- Short-term government bonds

- Regulated bank or government backed savings initiatives, preferably tax friendly

- Money market mutual funds

- National bonds (if living in a developed country)

- Stocks and shares on a trading platform

- Corporate bonds

Medium-term assets include:

- Physical property with focus on capital appreciation or REITs

- Equity and bond funds

- ETFs

- Structured notes

- Corporate bonds

Pensions and long-term assets include:

- Mutual funds – with focus on equities and bonds

- Physical property with a focus on high appreciation and rental income

- REITS

- Government backed, tax-free savings initiatives such as ISA in UK.

- Robo-advice accounts

Assumptions: Approximate age: 60 and retirement years

Hopefully now, by age 60 you have the option to wind down your workload, spending more time enjoying other pursuits and choosing to work as and when you need to. Your debts should by now be minimal and your mortgage repayments should be close to being cleared or cleared. With lower debt, you should still have a good disposable income, although this may be somewhat dented by clearing the last few bits of debt. Although the children maybe be older, if they are not already working and supporting themselves, the pressure on the bank of mum and dad may well be at its highest during these last few years of adolescence and early adulthood. Perhaps persuasion to take on an evening or weekend job will help instil the value of money and lessen the pressure on your own cash balance somewhat.

The focus now slowly moves towards taking account of all the money and assets you have built up and planning both their continued growth and how they will provide an income for when you decide to stop working. While accumulation of assets remains important, preservation and protection of your nest egg is as important. Your risk profile will have dropped to ensure that you are not exposing your assets to undue risk, which may dent your projected income potential and leave you waiting longer to retire.

When you have your retirement in sight, there is a need for another planning exercise to recalculate your spending needs. You may have done this some time ago when there was still uncertainty around your needs and how inflation may affect the cost. The magic formula will be to be able to see your assets grow in size at least to beat inflation while leaving them wisely invested in order to be able to draw an income from the value without seeing the capital fall behind inflation.

If the required income from your cash assets is USD50,000 per year, and the assets are valued at USD2.5 million, then a 4% yield will allow you to take USD50,000 as your income and leave USD50,000 to be fed back into or remain in the assets to combat inflation.

Real estate assets will work differently, and they should ideally be located where regular rental yields are achievable, even if this could mean lower growth of the property value.

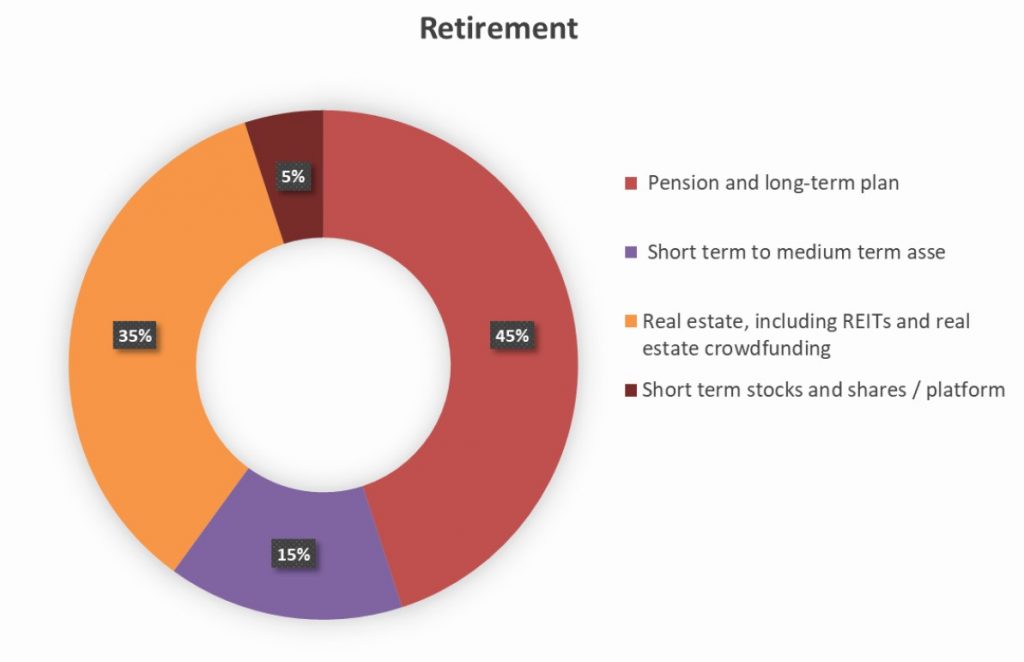

The chart below shows how your portfolio should typically be divided at this stage:

45% – Pension and long-term plan

15% – Short term to medium term assets (short 2-5 years, medium 6-12 years)

35% – Real estate, including REITs and real estate crowdfunding (excluding primary home)

05% – Short term stocks and shares / platform

Short-term assets include:

- Fixed interest accounts

- Lending clubs / peer-to-peer lending

- Short-term government bonds

- Regulated bank or government backed savings initiatives, preferably tax friendly

- Money market mutual funds

- National bonds (if living in a developed country)

- Stocks and shares on a trading platform

- Corporate bonds

Medium-term assets include:

- Physical property with focus on capital appreciation or REITs

- Equity and bond funds

- ETFs

- Structured notes

- Corporate bonds

Pensions and long-term assets include:

- Mutual funds – with focus on equities and bonds

- Physical property with a focus on high appreciation and rental income

- REITS

- Government backed, tax-free savings initiatives such as ISA in UK.

- Robo-advice accounts